Commercial real estate fundamentals continue to point to strong performance in the retail, multifamily, and industrial sectors with vacancy rates mostly declining on a year-over-year and quarter-to-quarter basis, robust rent growth, and positive excess demand. While there has been improvement in the office sector, the impact of work-from-home and the uncertainty surrounding near-term office usage continues to dampen performance.

Overall, the continued solid fundamentals reflect a healthy demand for commercial real estate across sectors. In the retail space, demand is driven by solid consumer behavior as households return to pre-COVID shopping and dining patterns. Meanwhile, retail supply remains muted.

In the industrial sector, there continues to be high demand as e-commerce logistics needs continue to grow. The continuing high levels of new supply appear to be catching up with net absorption in the industrial space.

Demand for multifamily space, while down from recent highs, continues to be well above historic averages and continues to outstrip historically high levels of new supply. Office markets experienced low, but positive, levels of net absorption that were outstripped by low level of new supply.

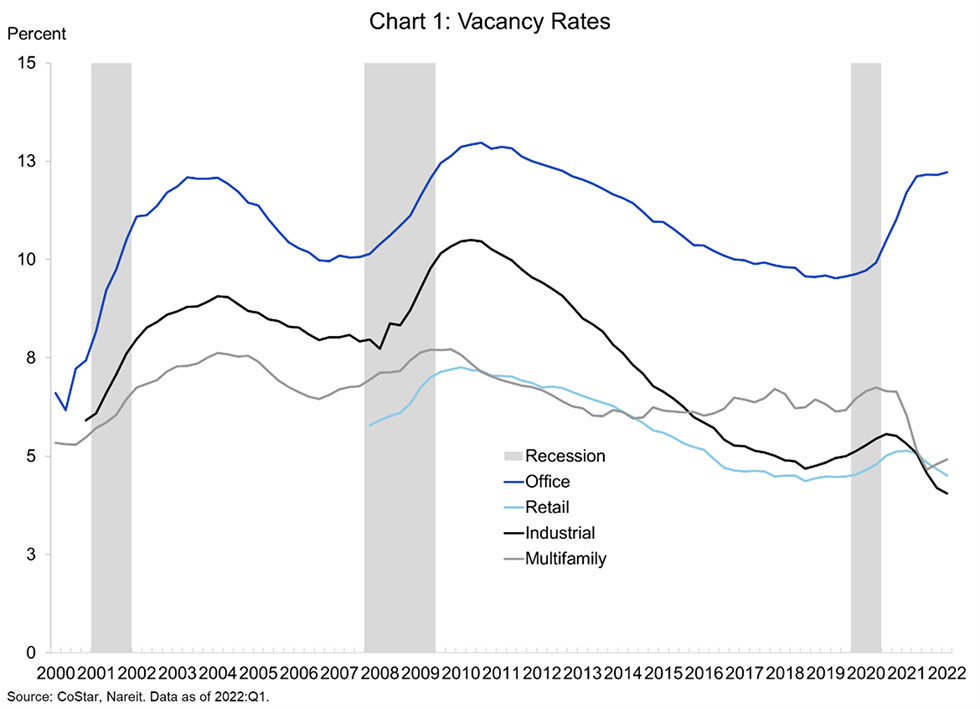

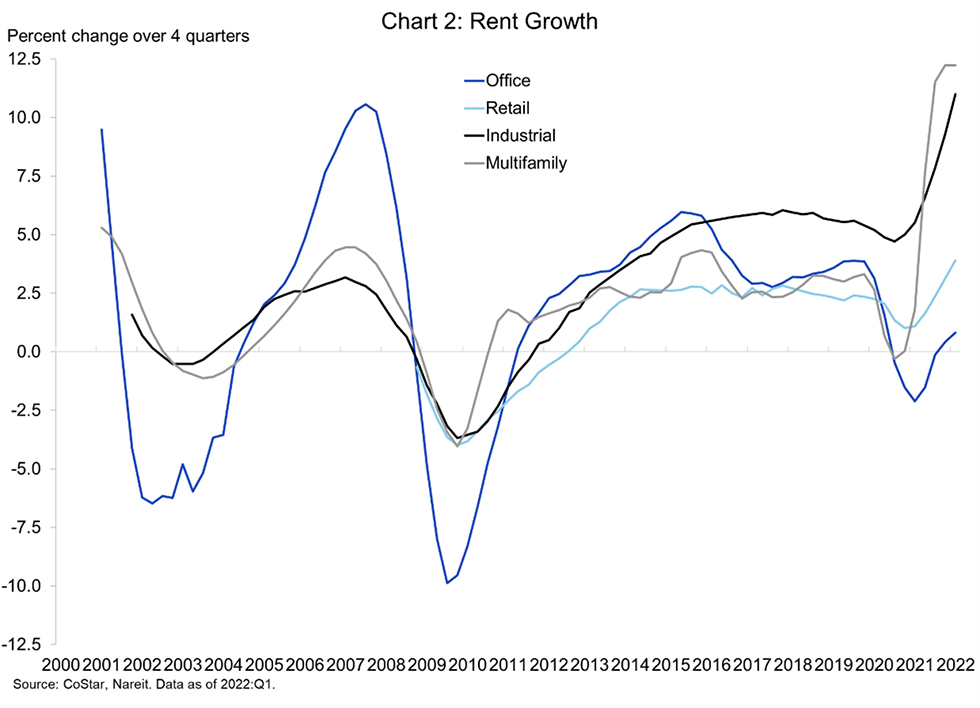

Vacancy Rates and Rent Growth

Vacancy rates fell in industrial and retail sectors, declining by 17 bps and 14 bps, respectively, to 4.1% and 4.5%. This is the lowest vacancy rate for the industrial sector on record and the lowest for retail since the third quarter of 2018. Apartment vacancy rates have ticked slightly higher to 4.9%, up 11 bps from the prior quarter and up 25 bps from its record low in the third quarter of 2021. Nevertheless, apartment vacancy rates are well below the historical average as they have been below 6% for the past four consecutive quarters. Prior to that, rates hadn’t been below 6% since 2001.

Office vacancy rates, in contrast, have stabilized as they have been essentially unchanged for the past four quarters following an increase of 200 bps over the prior year. Their current level of 12.2% is elevated above the pre-pandemic rate of 9.6% in the fourth quarter of 2019.

Rent growth accelerated for most property types. Apartment rents rose 12.2% compared to the first quarter of 2021, but leveled out compared with recent increases. Apartments are experiencing the highest rents and the highest rent growth on record.

Industrial rents rose 11.0% over the past four quarters and 3.2% from last quarter. The industrial sector is also experiencing its highest rents and rent growth on record.

Retail rents are steadily improving, increasing 3.9% over the past year and 1.2% over the past quarter. While growth is occurring at a slower rate than the multifamily and industrial sectors, retail rents are the highest they have ever been.

Office rents edged slightly higher compared to a year earlier, the second consecutive quarter of year-over-year increase since early 2020. While office rents growth has been recovering slowly, it remains well below pre-pandemic levels.

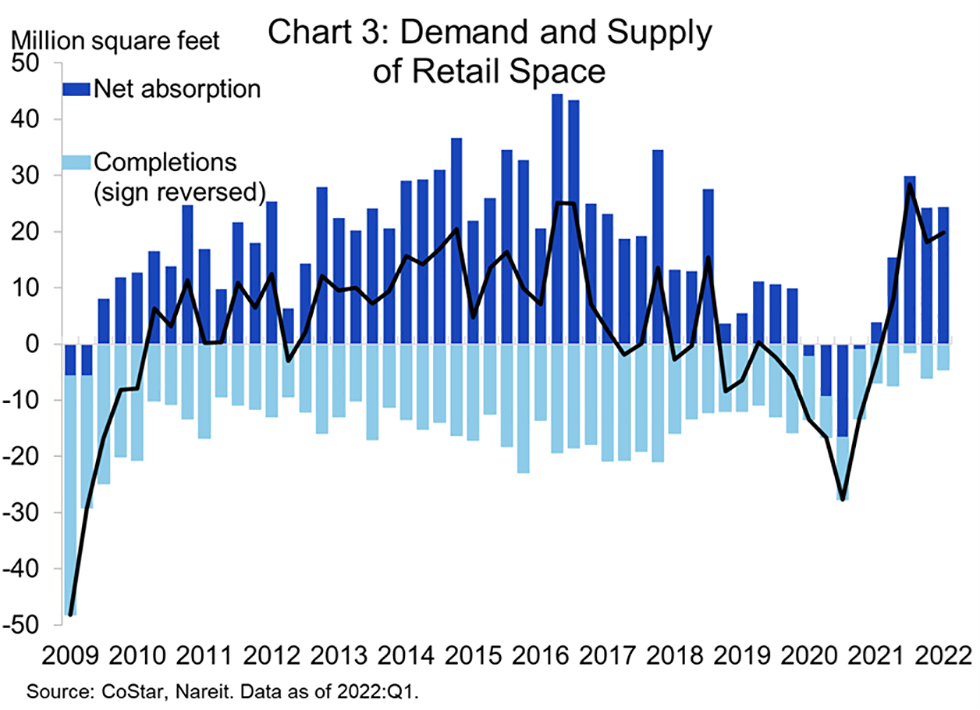

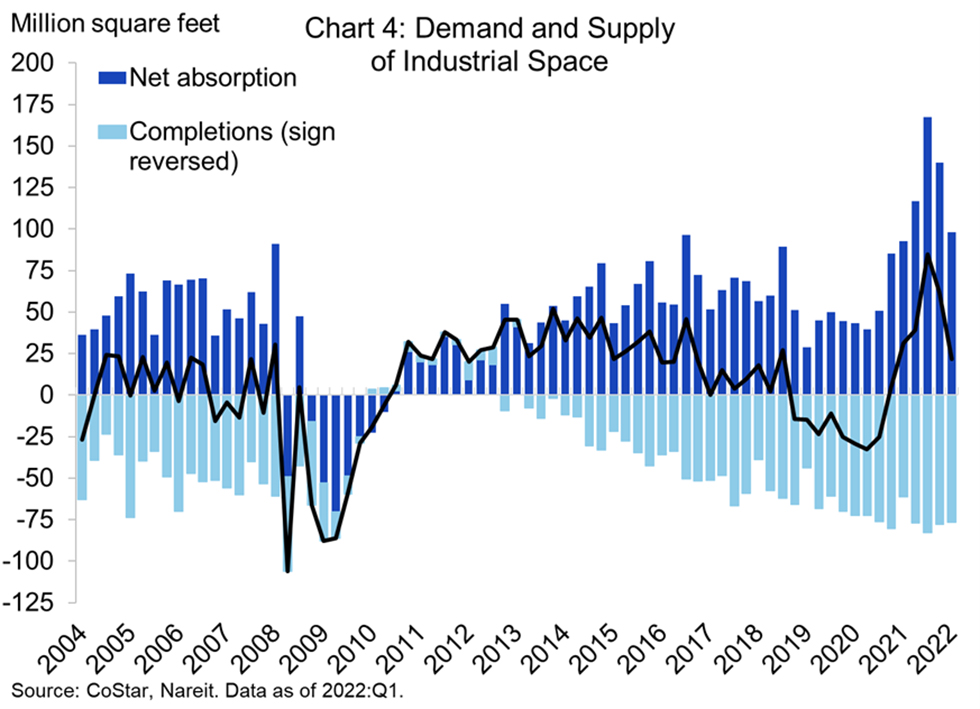

Demand and Supply

Following a quarter of robust demand growth in the commercial real estate market, excess net demand slowed in the first quarter of 2022 for most property sectors, but remains positive.

Retail properties saw the third consecutive quarter of robust demand and were the only sector with increased demand, with excess net demand rising 9.2% from the fourth quarter of 2021. Net absorption (i.e. growth in demand) was 24.4 million square feet. There continues to be very little new construction in the retail sector which has been the case throughout the pandemic.

Industrial markets had net absorption of 98.2 million square feet which is a sharp decline from the prior two quarters’ record levels, but still relatively high compared with historical averages. It fell 29.7% below the prior quarter’s level and 41.3% below the record level from the third quarter of 2021. A lack of available space may have kept demand from growing faster as industrial vacancy rates dropped 14 bps to a record low of 4.1%.

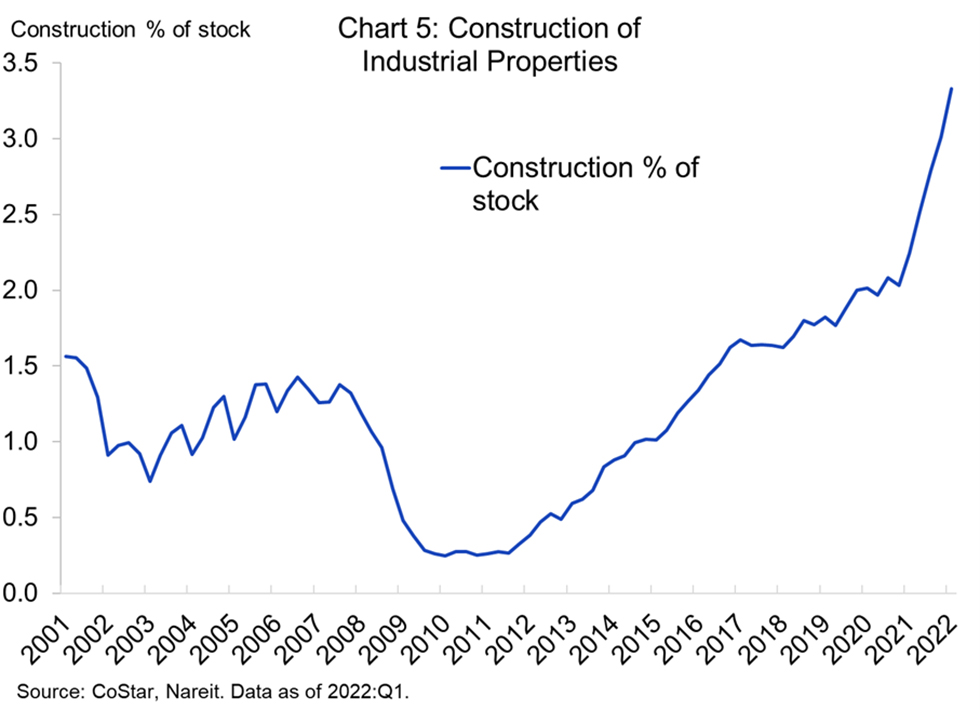

Industrial/logistics facilities are a key part of the supply chain, helping goods bought online get to the last mile delivery to consumers. Construction has surged during the pandemic, with nearly 590 million square feet of new facilities under construction. This is equal to 3.5% of the existing stock in the first quarter of 2021, up from the previous record high of 3.0% in the prior quarter. For comparison, construction activity was less than 1% of existing stock at a comparable point in the recovery from the 2008-2009 financial crisis.

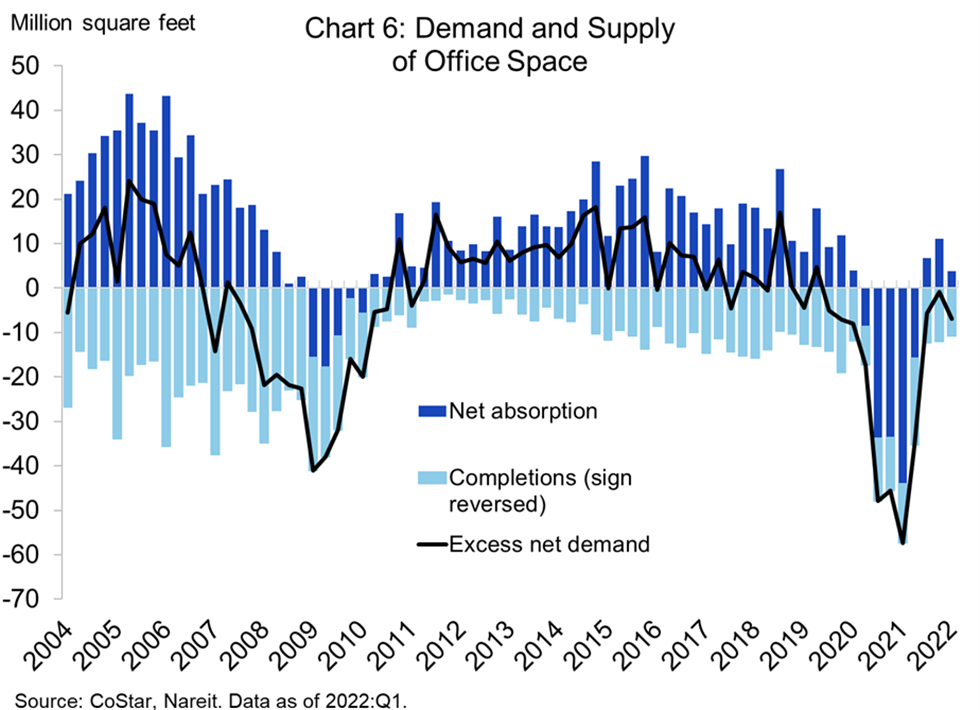

Office markets had 3.7 million square feet of net absorption in the first quarter which represents the sector’s third consecutive quarter of positive net absorption following five quarters of negative values during the pandemic. Supply continues to exceed demand in the office sector. This excess supply is indicative of the challenges facing the office sector due to the pandemic as vacancy rates are at their highest levels ever and many businesses continue to allow employees to work from home.

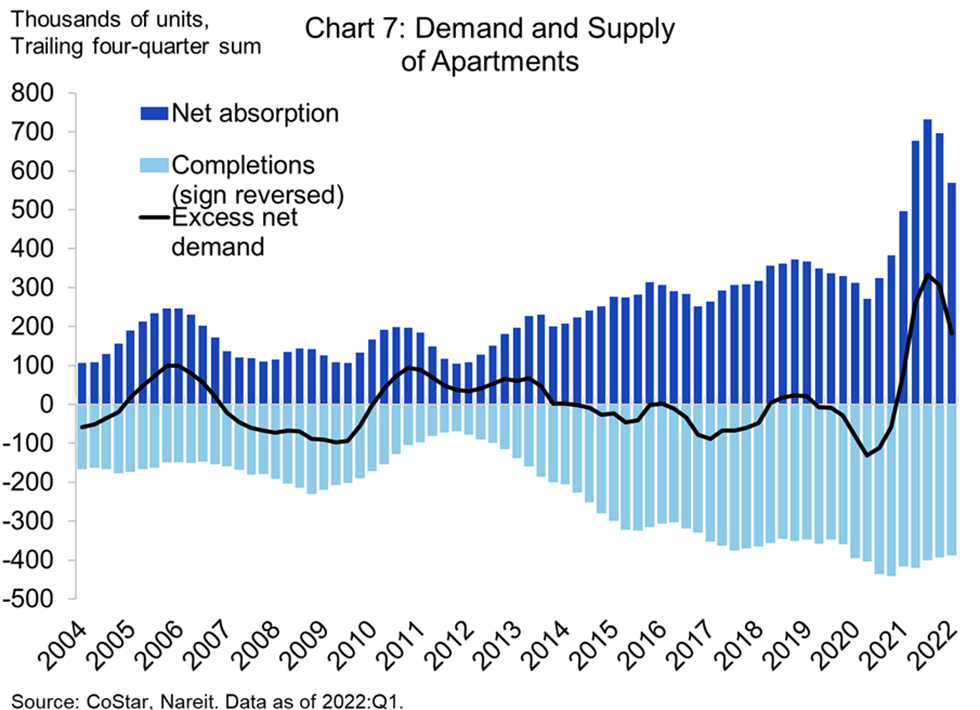

Multifamily demand eased for the second quarter in a row, to 58,000 units, from 62,500 in the fourth quarter. Low vacancy rates (making open apartments difficult to find) and rising rents creating affordability challenges could be contributing to this slowdown in demand. Net absorption over the past four quarters, which averages out seasonal differences, edged down from the prior quarter but demand continues to exceed new supply.