Nareit tracks quarterly investment holdings for the largest actively managed real estate investment funds focusing on REIT investment for insights into expert investor sentiment. In the fourth quarter of 2024, active managers continued to shift allocations to digital and health care sectors and away from commerce sectors.

Telecommunications and data centers were the most overweight sectors relative to their index weights, invested at 123% and 120% of their index shares, respectively. Health care jumped to the second highest absolute allocation in the fourth quarter, reflecting the largest year-over-year increase among the sectors. Industrial and retail were both down for the year and underweight their index shares by 88% and 86%, respectively.

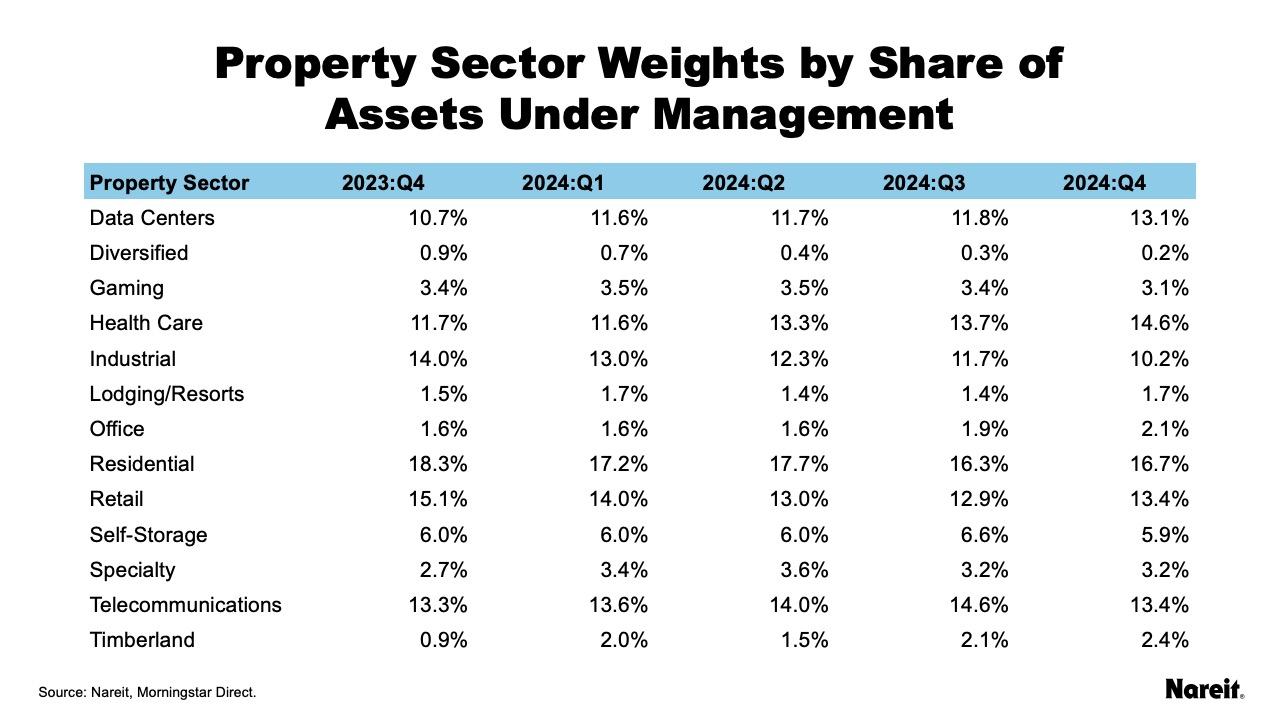

The table above shows the share of each equity REIT property sector by assets under management.

- Residential remains the property sector with the highest investment at 16.7%.

- Health care jumped to the second highest allocation at 14.6%, after moving into third place in Q2:2024.

- Retail and telecommunications essentially tied for third place at 13.4%, followed closely by data centers at 13.1%

- Diversified remained in last place at a 0.2% share.

- Office and lodging/resorts remained near the bottom of the distribution, but office had over a 2% share, with lodging/resorts remaining below 2%.

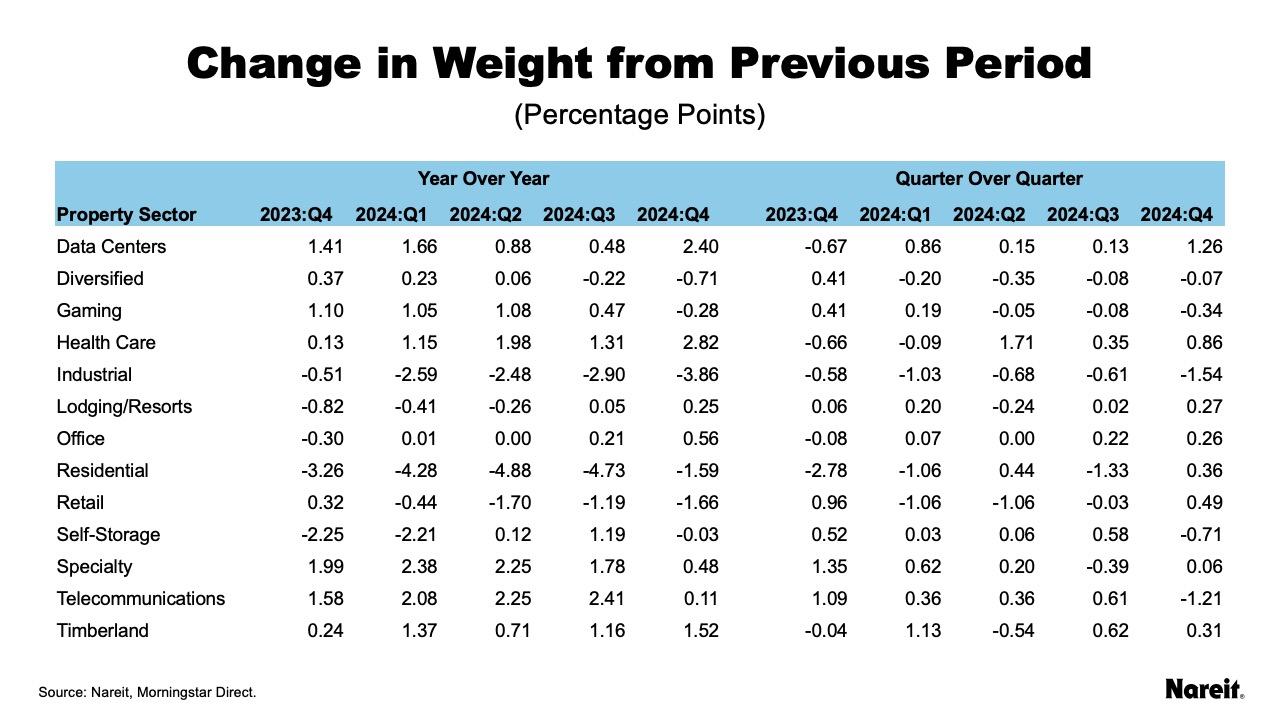

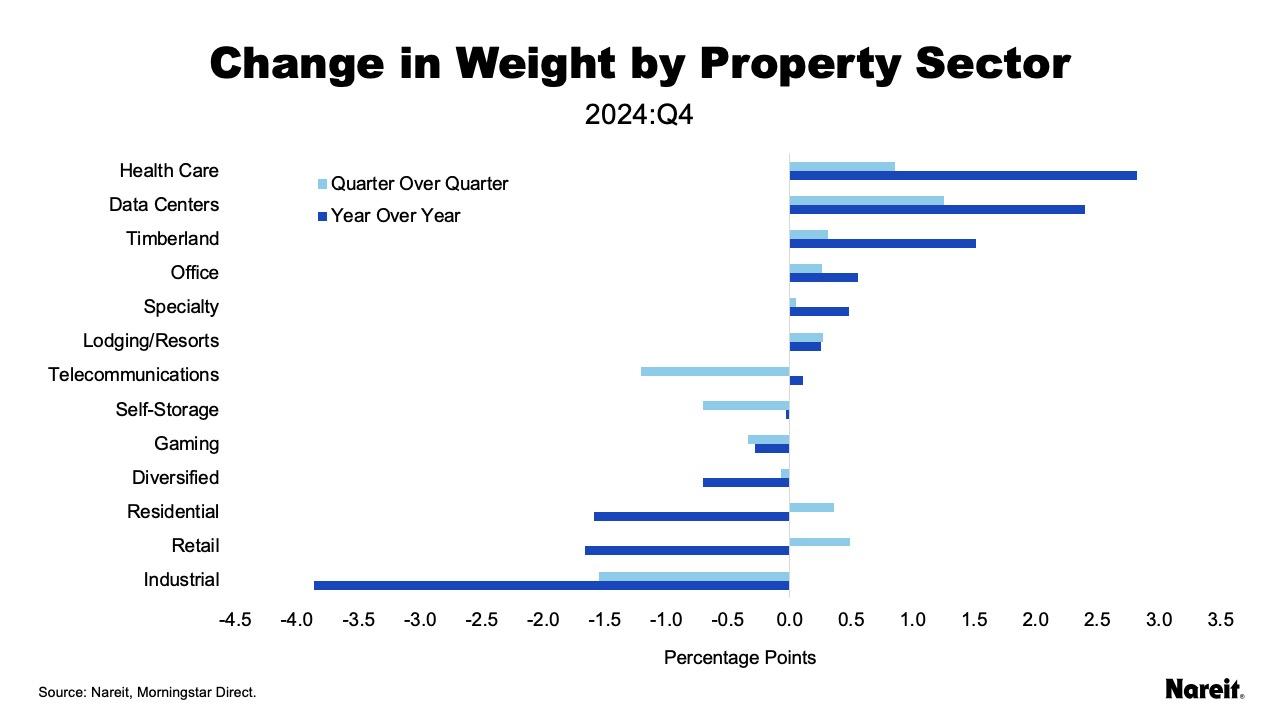

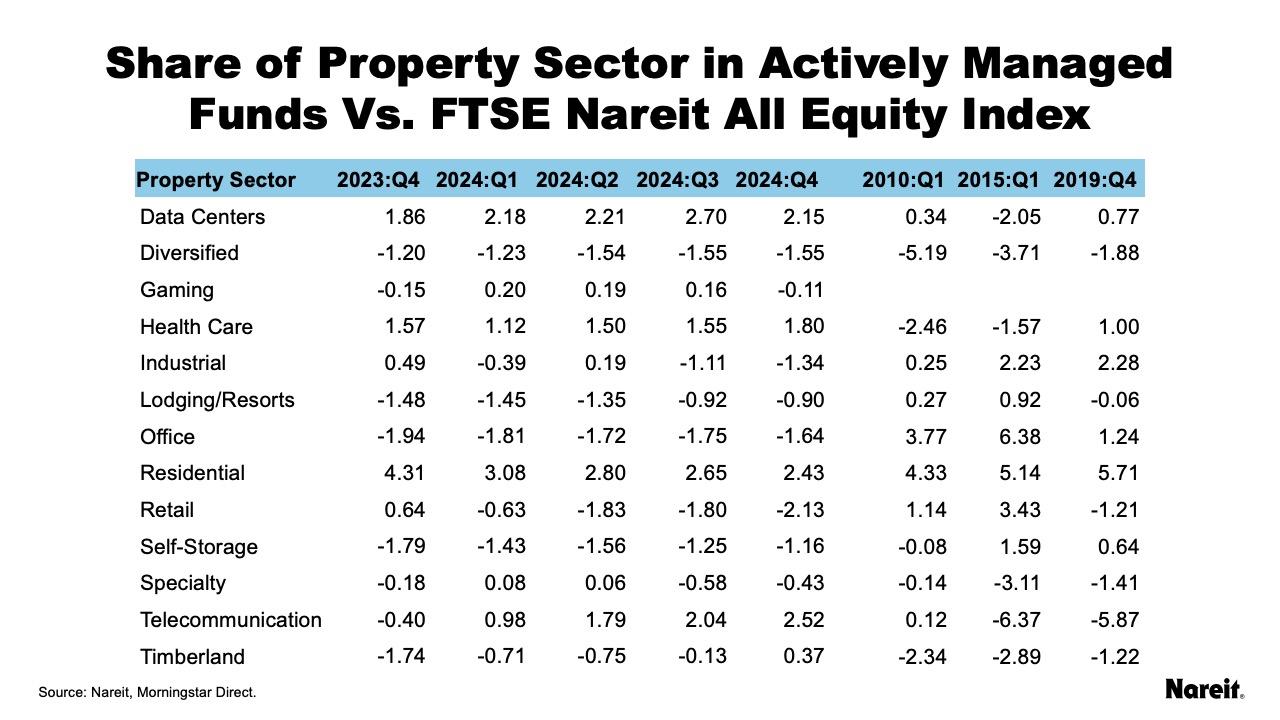

The table and chart above show the change in property sector asset share by quarter and from the previous year.

- Jumping into the second highest allocation spot, health care had the largest year-over-year increase, up 2.8 percentage points, and the second highest quarterly increase, up 0.9 percentage points.

- Data centers had the highest quarterly gain at 1.3 percentage points and the second highest annual gain at 2.4 percentage points, after two quarters of modest increases.

- A year of steady quarterly gains in the office sector resulted in a significant increase in annual gain, up 0.6 percentage points in the fourth quarter.

- Lodging/resorts also saw a turnaround, up 0.3 percentage points for the quarter and year.

- Reductions in industrial holdings continued in the fourth quarter, leaving the sector with the largest annual and quarterly decline, down 3.9 percentage points for the year and 1.5 percentage points for the quarter.

- Residential and retail saw steady decreases throughout 2024 in their share of funds, with residential down 1.6 percentage points and retail down 1.7 percentage points on a year-over-year basis. However, both saw small increases in the fourth quarter compared to the third, with residential up 0.4 percentage points and retail up 0.5 percentage points.

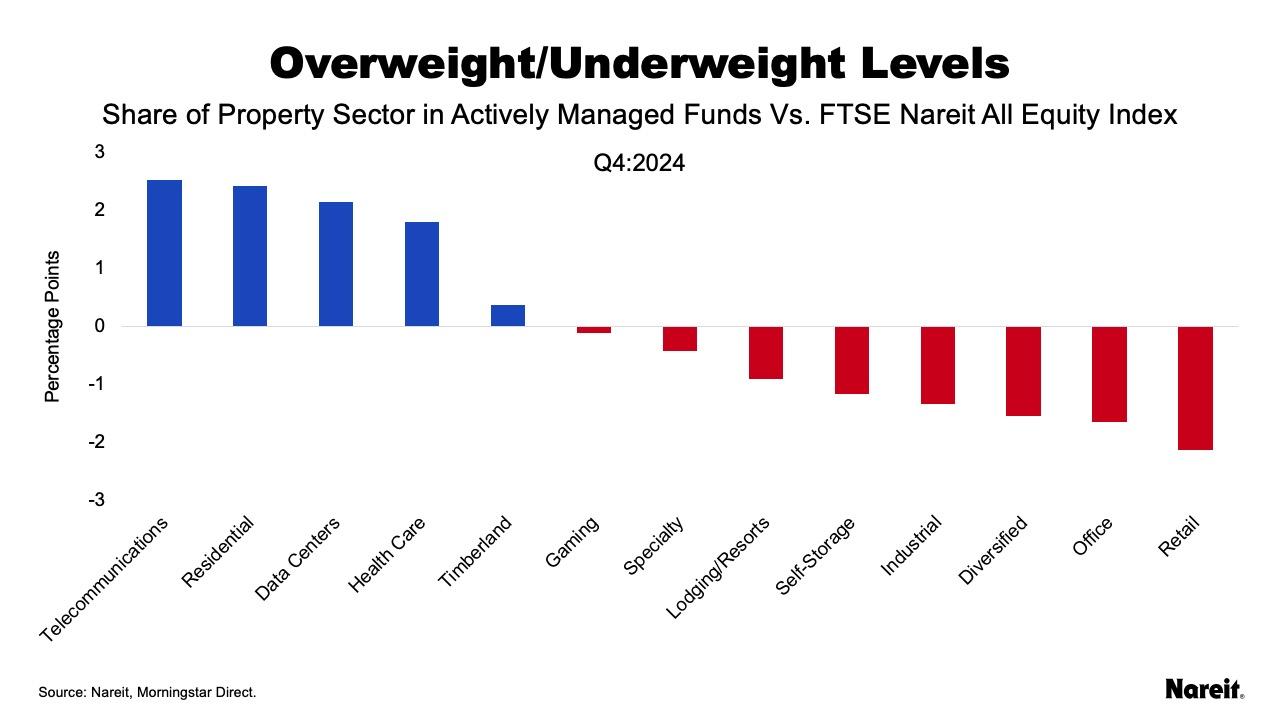

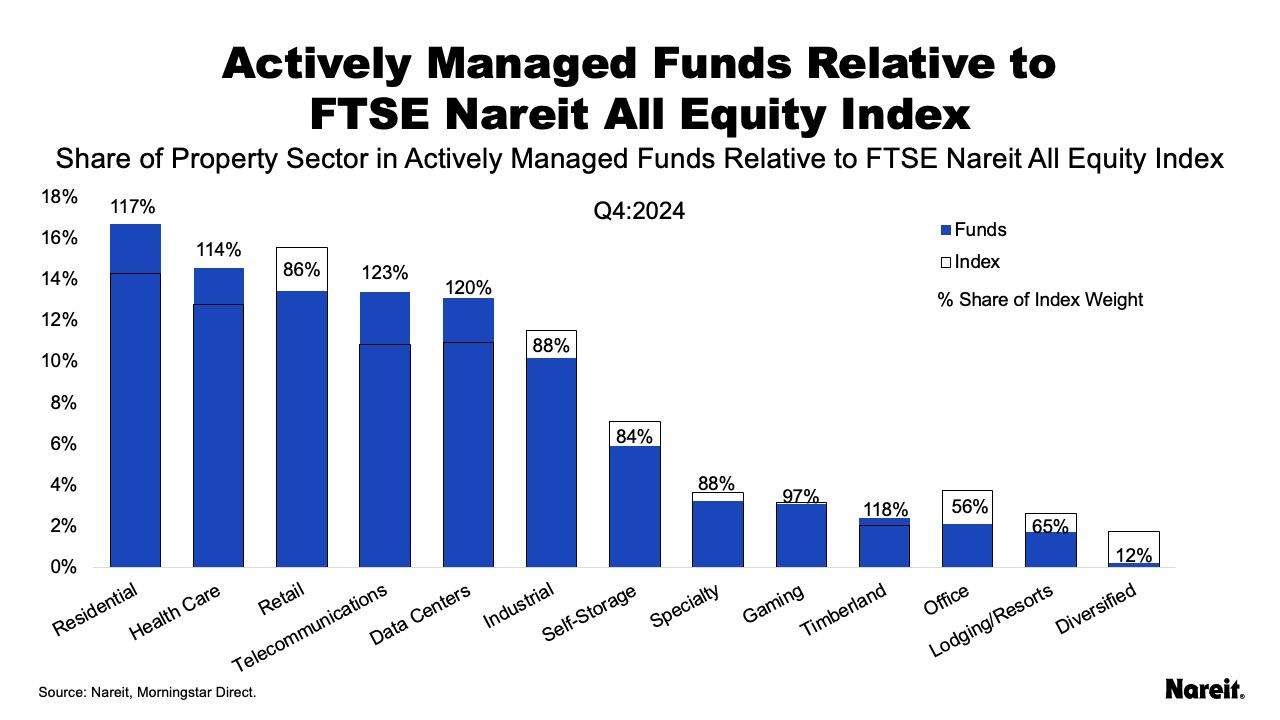

The charts and table above compare the weight of the sectors in actively managed funds to the weight of the sectors in the All Equity index.

- Funds remained strongly overweight in digital sectors through 2024. Telecommunications overtook data centers as the property sector with the highest overweight relative to its index share at 123%, followed by data centers at 120%. This is partly due to telecommunication’s share dropping in the index by 1.7 percentage points while data centers’ share increased by 1.8 percentage points. Thus, the denominator decreased for telecommunications and increased for data centers.

- Health care continued to be strongly overweight in 2024. After perennially overweighted residential and the digital sectors, health care was the most overweight by 1.8 percentage points or 114% of its index weight.

- Timberland jumped to overweight in the fourth quarter after being underweight the rest of 2024. At 118% of its index weight, timberland was the third most overweight sector by share of index weight.

- Retail and industrial were both underweight in the second half of 2024 (retail for the entire year). Both wereat less than 90% their index weights, with industrial underweight by 1.3 percentage points and retail underweight by 2.1 percentage points.

- Both office and lodging/resorts saw a steady gain in shares of index weights through 2024, although both remained significantly underweight. Lodging/resorts was less than a percentage point underweight in the fourth quarter, at 65% of its index weight. Office was still significantly underweight by 1.6 percentage points, or 56% of its index weight, but by comparison was at less than 45% at the end of 2023.

Note that six of the 26 funds had not reported fourth quarter data for this analysis.

For more information on the active manager project, see Reading the Real Estate Market: Tracking Active Managers’ Allocations Over Time.